- More

- Back

Taxbuzz | Vivad se Vishwas Scheme – Opportunity to settle tax disputes, now or never… March 11, 2020

Published in: TaxBuzz

Disclaimer: While every care has been taken in the preparation of this TaxBuzz to ensure its accuracy at the time of publication, Vaish Associates Advocates assumes no responsibility for any errors which despite all precautions, may be found therein. Neither this bulletin nor the information contained herein constitutes a contract or will form the basis of a contract. The material contained in this document does not constitute / substitute professional advice that may be required before acting on any matter. All logos and trademarks appearing in the newsletter are property of their respective owners.

• Eligible taxpayers under the Scheme:

Following taxpayers shall be eligible to avail the settlement/ benefit under the Scheme:

– Where appeal or writ or SLP filed by assessee or Department is pending as on 31.01.2020;

– Orders where time limit for filing appeal has not expired as on 31.01.2020;

– Case pending before DRP as on 31.01.2020 as well as cases where DRP had issued directions on or before 31.01.2020 but final assessment order has not been passed;

– Revision petitions pending before CIT under section 264 on 31.01.2020;

– Search cases where disputed tax is less than Rs. 5 crore (assessment year wise);

– Cases pending in arbitration in India or abroad.

Exclusions from the Scheme:

– Assessment year(s) of search cases if disputed tax is more than Rs 5 crore.

– Years in respect of which prosecution instituted under the Income tax Act on date of declaration.

– Tax arrears relating to undisclosed foreign income and assets.

– Tax arrears based on information from foreign countries as per section 90 or 90A.

– Persons against whom prosecution instituted on date of declaration under IPC or the Unlawful Activities Act, NDPS Act, 1985, PC Act, 1988, PMLA, COFEPOSA, Prohibition of Benami Property Transactions Act, 1988 and Special Court Trial in Securities Act, 1992.

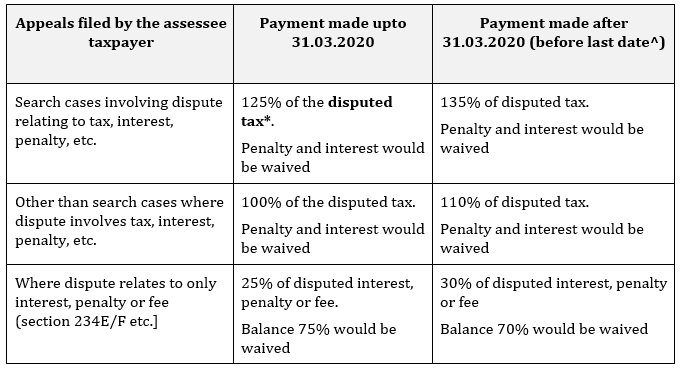

• Payment to be made under the Scheme:

^ last date to be specified by Central Government (tentative- 30.06.2020)*Disputed tax (including cess and surcharge)

a. Where any appeal, writ or SLP is pending before the appellate forum- amount payable as if such appeal or writ or SLP was to be decided against the assessee.

b. Where assessment order or order in appeal or writ has been passed and time limit for filing appeal or SLP has not expired as on 31.01.2020- amount of tax payable after giving effect to the order so passed.

c. Where objection filed is pending before the DRP- amount of tax payable if DRP was to confirm the proposed variations.

d. Where DRP has issued direction under section 144C(5) and the final assessment order is yet to be passed as on 31.01.2020- the amount of tax payable as per the final assessment order to be passed by the assessing officer pursuant to DRP directions.

e. Where revision application under section 264 is pending- amount of tax payable if such application was not to be declined.

f. Where enhancement issued by CIT(A) before 31.01.2020, disputed tax shall be increased by amount of tax pertaining to issues for which enhancement notice issued.

– Where dispute relates to reduction of loss or depreciation or tax credit under section 115 JAA or section 115D, option to the assessee either to:

(i) pay notional tax and carry forward related tax credit or loss or depreciation; or

(ii) forego the disputed credit or loss or depreciation without paying any tax.

– 50% of tax payable in following cases:

(a) Disputed tax relating to appeal/ writ/ SLP filed by the Department

(b) Issues on which there is favorable decision by ITAT/ HC.

– No tax payable on issue covered by SC in assessee’s own case

• Procedure under the Scheme:

– Assessee to file declaration in specified form before the Designated Authority (DA).

– Taxpayer to furnish an undertaking waiving his right to seek or pursue any remedy.

– DA to determine amount payable and grant a certificate within 15 days.

– Declarant to pay the amount within 15 days from the date of receipt of the certificate.

– Upon filing of declaration, pending appeal is deemed to have been withdrawn.

– Taxpayer to submit the proof of withdrawal of appeal or writ with intimation of payment.

– Appellate forums, arbitrator, conciliator or mediator shall not decide the issue in respect of cases where an order under clause 5(1) is passed by the designated authority.

– Amount paid in pursuance to the Scheme shall not be refunded under any circumstances

Clarifications/ Comments:

– Declaration form is to be filled assessment year wise, i.e., one declaration form for one year.

– Tax determined by DA – not appealable [FAQ No.47 of Circular 7/2020].

– DA has power to rectify patents errors in order/ certificate [FAQ No.46 of Circular 7/2020].

• Other important features of the Scheme

– Immunity from prosecution.

– Issues settled not to be concerned as any precedence

– If substantive addition is settled, protective addition shall go [FAQ No.35 of Circular 7/2020].

– No impact of settlement of TP adjustment on secondary adjustment made under section 92CE.

• Clarifications/ Comments:

– Draft order passed but no objection before DRP to await final order to file appeal before CIT(A): Assessee may opt for the scheme and pay tax as determined in the draft order.

– Disputes pending in AAR – Not covered.

– Writ pending against AAR ruling – Covered, with disputed tax to be computed as per AAR order [FAQ No.3 of Circular 7/ 2020].

– Issue set aside to the file of the assessing officer with a specific direction – Covered but assessee to also settle other issues arising in same appeal [FAQ No.7 of Circular 7/2020].

– Quantum appeal settled, penalty automatically deleted [FAQ No.8 of Circular 7/2020].

– Penalty appeal cannot be settled independently if quantum appeal also pending.

– Writ against 147 notice:

(a) Reassessment order not passed – Not covered [FAQ No.7 of Circular 7/2020].(b) If reassessment order passed – Covered (explicit clarification awaited).

– Issue wise settlement not possible – Entire appeal to be settled [FAQ No.14 of Circular 7/2020].

– Department appeal against ITAT order quashing assessment – 50% of disputed tax payable [FAQ No.14 of Circular 7/2020].

– Excess tax already deposited – to be refunded without any interest.

– Disputed tax to be computed considering rectification order passed by assessing officer.

– Option available to settle assessee and/ or departmental appeal [FAQ No.40 of Circular 7/2020]

– If TDS dispute is settled by the deductor, the deductee shall get the corresponding credit of taxes as on the date of settlement of dispute [FAQ No.30 of Circular 7/2020].

– On settlement of appeal against order u/s 201 (TDS default), no amount payable for settlement of issue relating to consequent disallowance u/s 40(a)(i)/(ia) [FAQ No.31 of Circular 7/2020].

– Where deductee settles dispute in respect of income on which TDS not deducted, deductor would not be required to pay TDS amount but only interest u/s 201 (1A). Deductor may also chose to settle the issue of such interest under the Scheme [FAQ No.32 of Circular 7/2020].

VA Comments and Open issues:

For any details and clarifications, please feel free to write to:

Mr. Rohit Jain : [email protected]

Mr. Deepesh Jain : [email protected]