Taxbuzz | The Taxation Laws (Amendment) Ordinance, 2019 September 25, 2019

Published in: TaxBuzz

Disclaimer: While every care has been taken in the preparation of this TaxBuzz to ensure its accuracy at the time of publication, Vaish Associates Advocates assumes no responsibility for any errors which despite all precautions, may be found therein. Neither this bulletin nor the information contained herein constitutes a contract or will form the basis of a contract. The material contained in this document does not constitute / substitute professional advice that may be required before acting on any matter. All logos and trademarks appearing in the newsletter are property of their respective owners.

With aim to provide fillip to the sluggish economy and promote growth and investment, the Government has by Ordinance made amendments in the Income Tax Act, 1961 (“the Act”) vide the Taxation Laws (Amendment) Act, 2019 which was promulgated by the President on 20.09.2019.

Key features of the aforesaid amendments are as under:

Section 115BAA – Lower tax rates introduced for domestic companies

- A new section 115BAA has been inserted w.e.f. assessment year 2020-21 which provides option to a domestic company to pay tax at lower rate of 22% (plus applicable surcharge and cess) as opposed to normal tax rate of 30%/ 25% (plus applicable surcharge and cess), provided the income is computed-

- without claiming exemption/ deduction

- u/s 10AA [SEZ units],

- u/s 32(1)(iia) [additional depreciation qua new plant and machinery @ 20%/ 30%],

- u/s 32AD [15% on new assets in undertaking set up in specified backward areas in Andhra Pradesh, Bihar, Telangana, and West Bengal]

- u/s 33AB [specified percentage of amounts deposited with Tea/ Coffee/ Rubber Board]

- u/s 33ABA [specified percentage of amounts deposited in Site Restoration Account]

- u/s 35(1)(ii)/(iia), 35(2AA) [specified deduction for scientific research]

- u/s 35AD [expenditure on specified business]

- u/s 35CCC [expenditure on agricultural extension project]

- u/s 35CCD [expenditure on skill development project]

- under Part C of Chapter VIA except section 80JJAA of the Act (such as 80IA/ IB/ IC/ ID/ IE etc.)

- without set-off of any brought forward losses to the extent such loss relates to deductions mentioned above. Such losses would also not be allowed to be carried forward to subsequent years.

- after claiming depreciation other than additional depreciation u/s 32(1)(iia).

- Benefit of lower rate under the aforesaid section can be exercised by the company from any year commencing from AY 2020-21 or onwards. Such option is to be exercised in prescribed manner, before due date of return u/s 139(1) for the year in which option is exercised. Option once exercised would be binding for subsequent years and cannot be withdrawn.

Observations/ Comments:

- Effective tax rate u/s 115BAA would be 25.168% (including 10% surcharge and 4% cess). Surcharge in respect of income chargeable to tax under section 115BAA is prescribed @ 10%.

- Benefit is available only to domestic companies and not to other categories of assessee like partnership firm, LLP, foreign company etc.

- Domestic company will have to weigh the benefit of lower rate under this provision with effective tax rate under existing scheme arrived after taking specified deduction(s)/ exemption(s). If the benefit on accounts of deduction u/s 10AA or additional depreciation or under Chapter VIA (Part C) etc. are expected to be substantial over the years, the domestic company may choose not to exercise such option. Option u/s 115BAA in such cases may be exercised later when benefit of such deductions/ exemption recedes.

- Only brought forward losses attributable to specified deductions/ exemptions are not allowable. Other brought forward losses and unabsorbed depreciation u/s 32(2) are allowed to be set off.

Section 115BAB – Lower tax rates introduced for domestic manufacturing companies

- New section 115BAB has been inserted w.e.f. assessment year 2020-21 which provides option to a domestic manufacturing company to pay tax at a lower rate of 15% (plus applicable surcharge and cess) if such company is set-up and registered on or after 1st October, 2019 and commences manufacturing activity upto 31st March, 2023.

- Surcharge in respect of income chargeable to tax under section 115BAA is prescribed @ 10%.

- Akin to the provisions of section 115BAA, income for the purposes of the aforesaid preferential rate has to be computed without claiming exemptions / deductions, set-off of brought forward losses, as prescribed in that section and discussed above.

- Additionally, following conditions must be fulfilled by the company to avail benefit of lower tax rate:

- company must not be formed by splitting up, or the reconstruction of a business already in existence;

- company must not use machinery or plant previously used for any purpose. Used plant and machinery to the extent of 20% of total value of plant and machinery is permissible;

- company must not use building previously used as a hotel or a convention centre.

- Similar to provisions of section 80IA(10), sub-section (4) of section 115BAB empowers the assessing officer to determine/ deem reasonable profits of such domestic company, if such company has business arrangements or enters transaction with connected parties in a manner that it produces more than ordinary profits. Domestic transfer pricing provisions contained in section 92BA have been made applicable to transactions of eligible companies with connected parties.

- Akin to provisions of section 115BAA, if company opts for lower rate of tax given under this section, it shall not be able to subsequently withdraw the option.

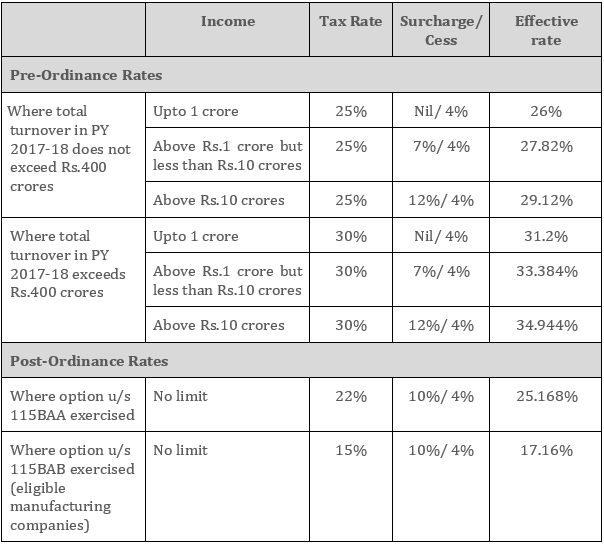

- Comparative tax rates for assessment year 2020-21 pre and post the Ordinance for domestic companies are as under:

Section 115JB – Reduced tax on book profit of companies not claiming benefit u/s 115BAA/ 115BAB

- Provisions of section 115JB have been amended to reduce the Minimum Alternate Tax (MAT) on book profit from 18.5% to 15%, w.e.f. assessment year 2020-21.

- Companies availing benefit of lower tax rate under new provisions of sections 115BAA/ 115BAB have been exempted from MAT on book profit under section 115JB.

Observations/ Comments:

- Considering that section 115JB shall not be applicable to companies opting for tax under the new provisions of sections 115BAA/ 115BAB, the issue whether brought forward MAT credit u/s 115JAA shall be available for set off against the tax liability under the new provisions would be contentious.

Section 115QA – Tax on buyback of shares

- Section 115QA was inserted vide Finance Act, 2013 providing for 20% tax in the hands of domestic company on ‘distributed income’ to the shareholders on buyback of unlisted shares.

- The aforesaid section was amended by the Finance (No.2) Act, 2019 to also include buy back of shares listed on a recognised stock exchange.

- Since the aforesaid amendment was brought in the middle of the year through the interim budget (Finance No.2) Act, 2019 on 05.07.2019, the same was considered to be harsh for listed companies which had on the basis of the existing provisions of no buy back tax, announced buy back of its shares prior to promulgation of the aforesaid new provision.

- As a measure of relief to such companies, section 115QA has been further amended to exclude transaction of buy-back of listed shares announced before 5th July, 2019.

Rationalization of surcharge

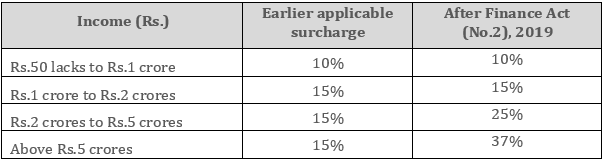

- Vide Finance Act (No.2), 2019, surcharge on income tax was increased for individuals, HUF, BOI, AOP and artificial judicial person falling in higher income bracket in the following manner:

- The aforesaid higher surcharge of 25% and 37% introduced vide Finance Act (No.2), 2019 has been removed for-

- Foreign Institutional Investors (FIIs) deriving income by way of capital gains from transfer of securities covered under section 115AD (1)(b);

- individuals, HUF, BOI, AOP and artificial judicial person deriving income by way of capital gains on transfer of equity shares or units of equity-oriented funds (covered u/s 111A and 112A) .

- Unlike individuals / HUF, BOI, AOP the benefit of lower surcharge to FIIs covered under section 115AD(1)(b) is available on capital gains from transfer of all securities like debt oriented funds and not just equity/ equity oriented funds.

- Withdrawal of higher surcharge would encourage/ boost investments in capital investments.

CBDT Circular- High Depreciation on Motor Vehicles

- With intent to provide boost to ailing automobile sector, new higher rates of depreciation have been notified by CBDT for motor cars/ vehicles acquired on or after 23rd August, 2019 and before 1st April, 2020 and put to use by that date:

- For motor-cars other than those used in a business of running them on hire, rate of depreciation is enhanced to 30% as against existing rate of 15%;

- For motor buses, motor lorries and motor taxis used in a business of running them on hire, rate of depreciation is enhanced to 45% as against existing rate of 30%.

For more information please write to:

Mr. Gaurav Jain at [email protected]

Mr. Deepesh Jain at [email protected]